Talk to The Behavior Gap like its author wrote you back.

Get the ideas that fit your life — not generic summaries.

- Chat with the book

- Audiobook-style main ideas

- Adapts to your life and goals

- Helps you take action

The Behavior Gap, in detail

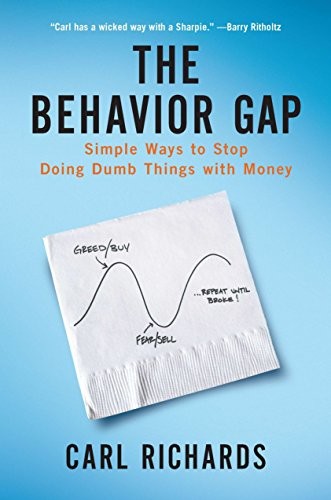

The Behavior Gap names a specific problem: the gap between what we know we should do with our money and what we actually do. Carl Richards, a certified financial planner and the author of the New York Times "Sketch Guy" column, illustrates this gap with simple diagrams throughout the book. The signature sketch — a Venn diagram where "what we should do" and "what we actually do" barely overlap — captures the book's central concern in a way that most financial writing fails to do in hundreds of pages.

Richards is not interested in technical finance. He assumes readers know the basics: diversify, save more, spend less, avoid timing the market. His argument is that knowledge is not the problem. The problem is behavior under emotional pressure. Investors sell at the bottom because the pain of watching a portfolio decline becomes unbearable. They buy at the top because they see friends making money and FOMO overwhelms their long-term plan. They make major financial decisions — buying a house, choosing a job — to impress people they don't particularly like.

The book is organized around the most common behavioral traps: confusing complex products with sophisticated strategy, mistaking activity for progress, ignoring the difference between what matters and what feels urgent. Richards draws on his own mistakes as much as his clients' — including a period when he and his wife owned a house they couldn't afford and had to short-sell it. The honesty distinguishes the book from advice that comes from people who've never made a consequential financial error.

The limitation is scope. The Behavior Gap is short, accessible, and clear, but it doesn't go deep. Readers wanting a rigorous behavioral finance treatment will need Kahneman or Thaler. What Richards offers is a practical, empathetic reframe: most financial problems are not knowledge problems, and solving them requires looking honestly at the emotional responses driving your decisions.

The big ideas

- 1.

The behavior gap is the distance between the returns the market earns and the returns investors actually capture — driven by buying high and selling low at emotionally charged moments.

- 2.

Most financial problems are not caused by lack of information. They are caused by acting on fear, greed, or the desire to appear sophisticated when you should be doing nothing.

- 3.

Complexity is often sold as sophistication, but a simple, well-understood plan consistently executed beats a complicated strategy executed poorly.